How to opt out of prescreened offers in 2026

Being behind major reports like The Mother of All Breaches and RockYou2024, our in-house cybersecurity experts and journalists provide unbiased, real-world testing and in-depth analysis.

We maintain complete transparency by openly sharing our testing methodologies with our audience.

Learn more

The credit card mailers, insurance pitches, and loan offers addressed to you by name – they keep showing up, but you never signed up for any of it.

They arrive because the four major credit bureaus – Equifax, Experian, TransUnion, and Innovis – are legally allowed to sell your financial profile to creditors and insurers under the Fair Credit Reporting Act (FCRA).

The good news is that opting out takes about 2 minutes online and costs nothing. It's your legal right, and the process is simpler than most people expect.

The catch – and there's always one – is that this opt-out only covers one corner of a much bigger problem. This guide walks you through every method and explains what to do about the rest.

What are prescreened offers?

Prescreened offers – sometimes called preapproved offers – are credit card, loan, and insurance solicitations sent to people who match criteria a creditor set in advance.

Think of it like a filter. A credit card company decides it wants customers with a credit score above 680. It pays a bureau to run that filter across millions of consumer files and send back a matching list. You're on that list. You didn't agree to be on it. You just happen to fit the profile.

That's the business model behind every "pre-approved" offer you've ever received. Under the FCRA, this is legal. Credit bureaus are permitted to share your information for "firm offers of credit or insurance." Opting out removes your name from those lists before the filter even runs.

These offers also generate soft inquiries on your credit report – visible only to you, not to lenders, and not factored into your score. But they do mean creditors are regularly peeking at your financial profile without your knowledge or consent.

How to opt out of prescreened offers

You've got 3 options: online for 5 years or permanently by mail and phone. The free methods are genuinely quick. But before we get to those, there's one thing worth knowing about first.

Pay attention to data brokers

Here's the honest version: OptOutPrescreen.com handles the credit bureau pipeline. That's it. Your data still lives with hundreds of data brokers, people-search sites, and marketing aggregators that the FCRA opt-out doesn't touch.

If you want to close both gaps at once, that's what automated data removal services do. For example, Incogni automatically sends legally valid removal requests to 420+ data brokers on your behalf – people-search sites, marketing databases, health data aggregators, and more. It resubmits them every 60–90 days because brokers have a habit of quietly re-adding you after the initial removal.

Here's how to get started:

-

Sign up on Incogni's website and provide the minimal data needed to find your exposed profiles.

-

Sign the authorization form to grant Incogni legal permission to contact data brokers on your behalf.

- Let Incogni run. It scans for your profiles, sends removal requests automatically, and keeps working in the background – no manual follow-up needed.

For best effects, pair Incogni or any other data removal service with the prescreened opt-out below. Together, they cover both channels. On its own, each one leaves a gap.

If you want to see which brokers already have your data before committing, Incogni's Digital Footprint Checker shows you exactly where your data is exposed.

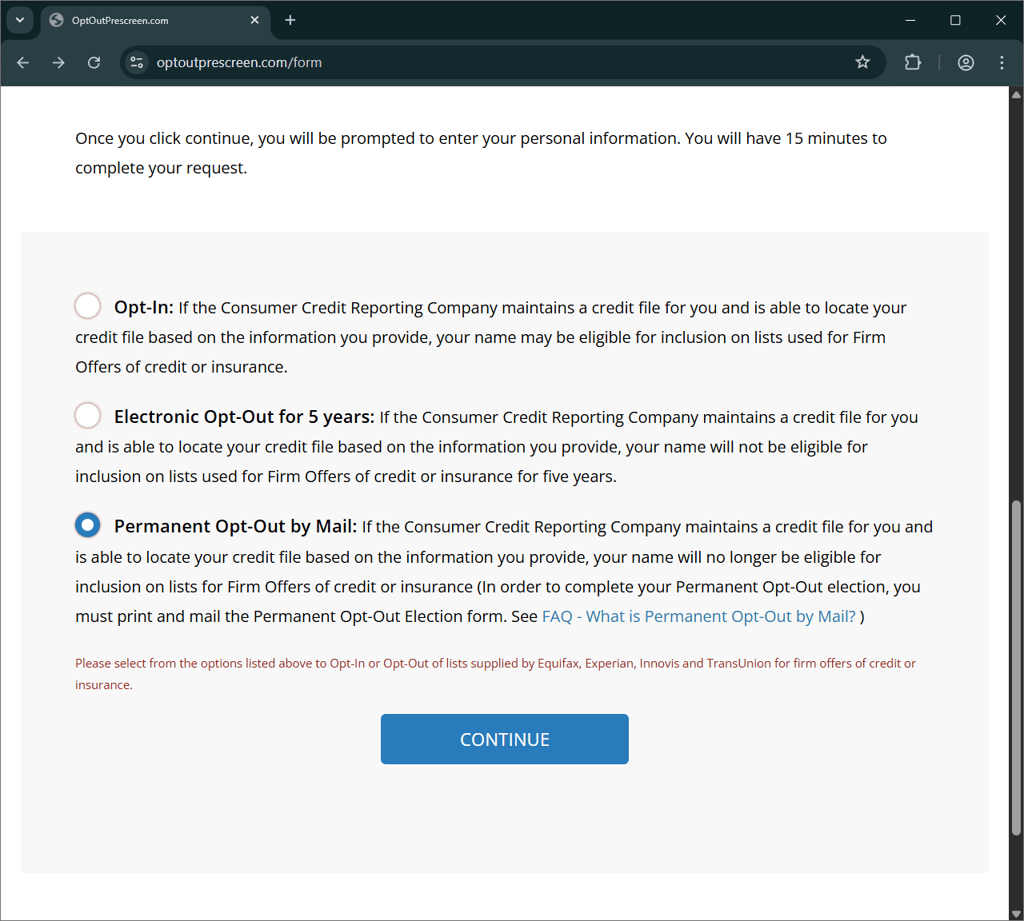

Opt out online (5 years)

This is the fastest free route. OptOutPrescreen.com is the only site the four major bureaus have authorized for this under the FCRA – any other website claiming to do the same isn't the real thing. Here’s what you need to do:

-

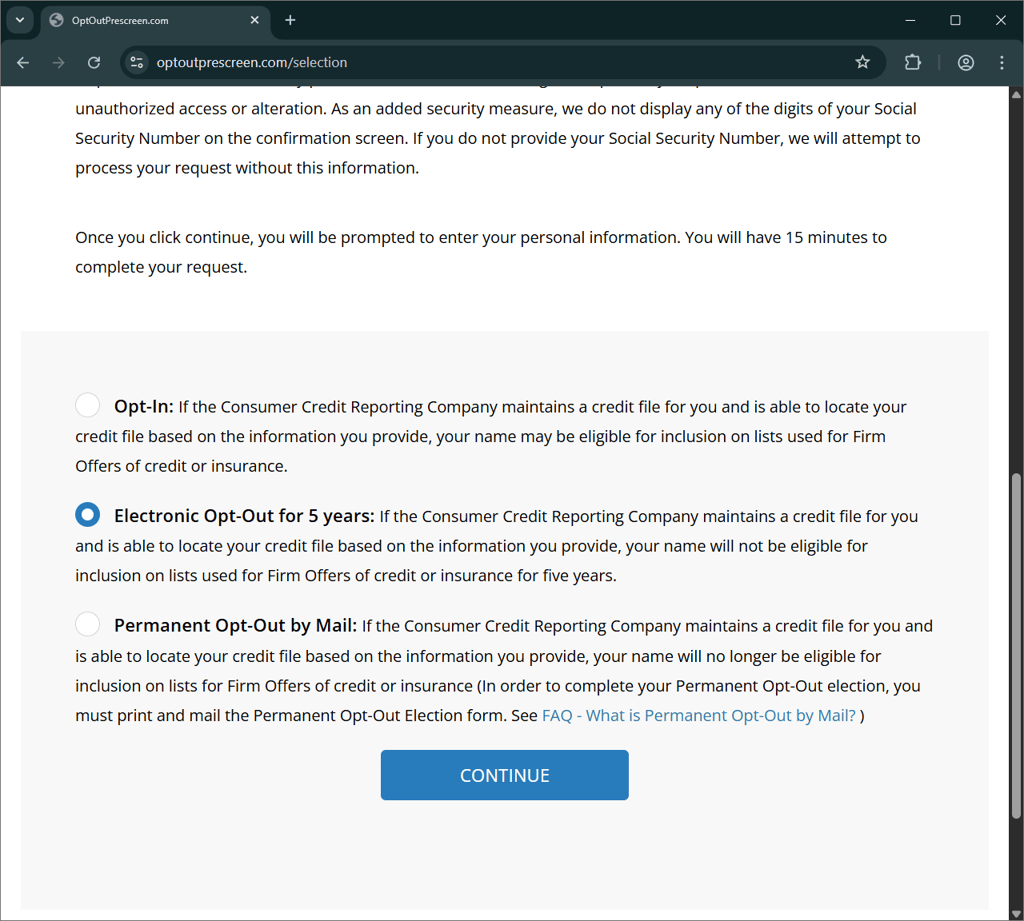

Go to optoutprescreen.com, scroll to the bottom of the page, and click on Click here to opt-in or opt-out.

-

Select Electronic Opt-Out for 5 years from the options.

-

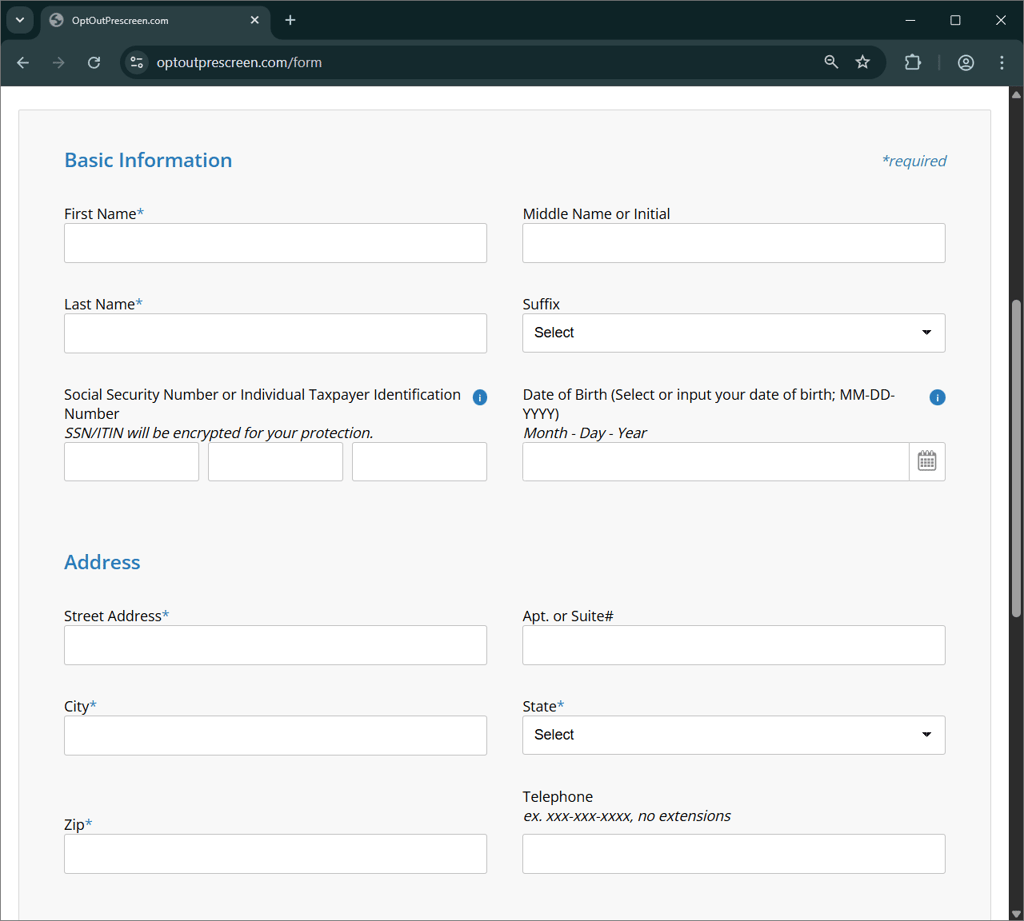

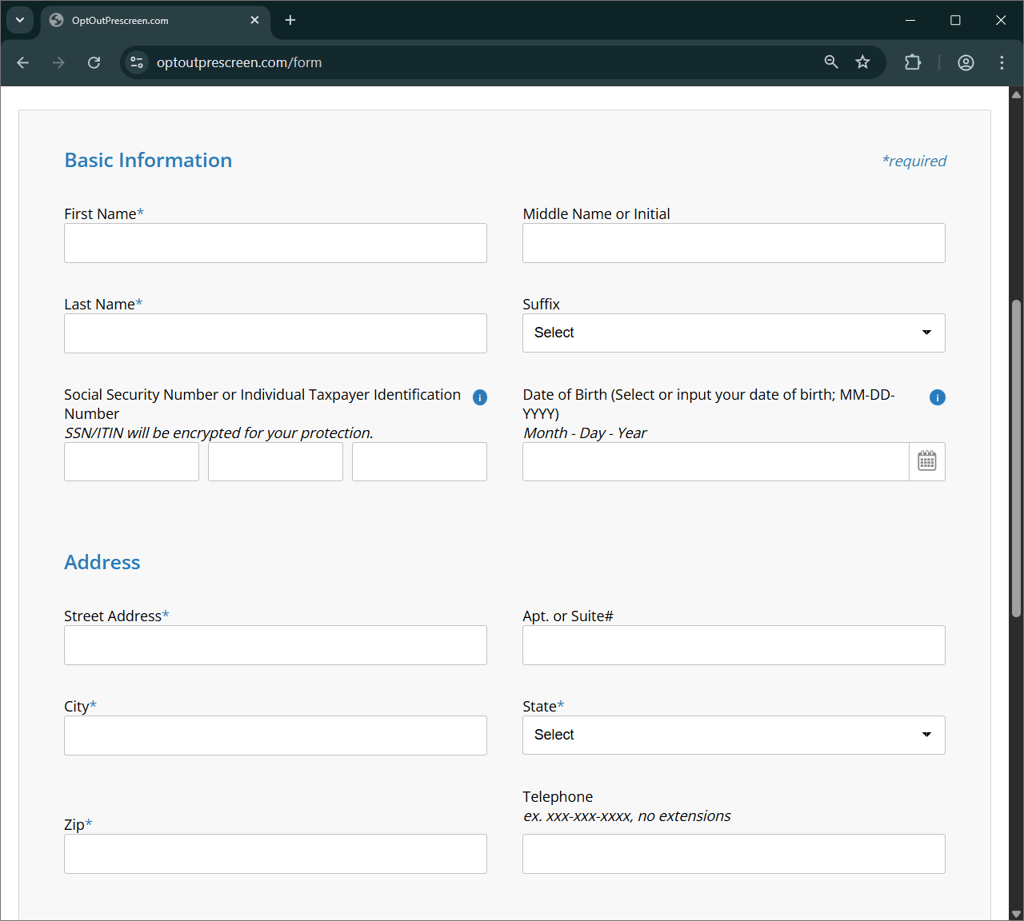

Enter your details: first name, last name, and current address. Date of birth and Social Security number are optional but improve matching accuracy.

-

Submit your request. Processing takes 5 business days. Allow up to 60 days before the mail stops – offers already in the pipeline will still arrive during that window.

Opt out permanently (mail-in)

The permanent option doesn't expire. The tradeoff: you'll need to finish it with pen and paper – a small inconvenience for something that lasts forever. Here are the steps you need to follow:

-

Go to optoutprescreen.com, scroll to the bottom of the page, and click Click here to opt-in or opt-out.

-

Select Permanent Opt-Out by Mail.

-

Enter your details: first name, last name, and current address. Date of birth and Social Security number are optional but improve matching accuracy.

- When you submit your request online, you'll get a confirmation – print it along with the Permanent Opt-Out Election Form.

- Sign the form physically. A physical signature is legally required – the electronic route only gets you 5 years.

- Mail the completed form to the address listed on the form. Once they receive it, they'll process your request.

Opt out by phone

The phone option works just as well. Call 1-888-567-8688 (1-888-5-OPT-OUT) – the official number operated by all four major bureaus. The automated system walks you through both the 5-year and permanent options.

Is OptOutPrescreen.com legitimate?

The site looks like it hasn't been updated since 2007, which may seem like a red flag. However, it's legitimate.

OptOutPrescreen.com is the only channel authorized for this purpose. The FTC references it, the CFPB references it, and Equifax, Experian, TransUnion, and Innovis all link to it from their own websites. The dated design is a feature of government-adjacent infrastructure.

A few things worth keeping straight:

- The real site is OptOutPrescreen.com only. Any variation or alternate domain isn't it.

- It will never proactively call or email you. Unsolicited contact claiming to be from OptOutPrescreen.com is a scam.

- The official phone number 1-888-567-8688 is verified by the FTC and listed on all four bureau websites.

Opting out of prescreen offers doesn't cover everything

OptOutPrescreen.com pulls you off the lists the credit bureaus sell to creditors and insurers. That's a meaningful, worthwhile thing to do. But it ends there.

The FTC says it plainly: the opt-out stops only prescreened offers based on credit bureau lists. But your information is still sitting with:

- People search sites (Spokeo, BeenVerified, Whitepages, and hundreds more)

- Marketing data aggregators (Acxiom, Epsilon, and others)

- Direct mail brokers that don't use the bureau pipeline

- Recruitment and background check databases

None of that is touched by the FCRA opt-out. Each broker runs on its own rules, with its own removal process.

Our recommended approach: do the prescreened opt-out yourself, then use Incogni to handle the rest. It sends automated removal requests to 420+ data brokers, re-submits every 60–90 days, and keeps working long after you've stopped thinking about it.

Conclusion

Opting out of prescreened offers is one of the easiest privacy wins out there – two minutes, zero cost, and your legal right. Do it today if you haven't. What it won't do is make your data disappear from the internet. The data broker ecosystem runs on its own terms, and OptOutPrescreen.com doesn't reach it.

Instead of focusing on one, do both. The prescreened opt-out handles the credit bureau side, while Incogni handles everything else – automatically, repeatedly, without you having to think about it again.

FAQ

Is it safe to give my SSN to OptOutPrescreen.com?

Yes, it’s safe to give your SSN to OptOutPrescreen.com. The site asks for it because the bureaus already have your SSN on file, and providing it just helps them match your request to the right record faster. However, the SSN field is optional – you can skip it, and your opt-out still goes through.

Does opting out affect my credit score?

Opting out doesn't affect your credit score at all. Prescreened inquiries show up as soft inquiries – visible only to you, not to lenders, and not factored into any scoring model. Equifax has confirmed that opt-out decisions won’t affect your credit rating.

How long does the prescreened opt-out take to work?

The prescreened opt-out request processes within 5 business days. But getting the mail to actually stop takes up to 60 days – offers already in the production and mailing pipeline will keep arriving during that window. If you're still getting prescreened offers after 60 days, something's off, and it's worth contacting the bureaus directly.

Can I opt back in after opting out?

Yes, the opt-out is completely reversible. Visit OptOutPrescreen.com or call 1-888-567-8688 at any point – the process runs exactly the same way in reverse.

Does opting out stop all junk mail?

No, opting out doesn’t stop all junk mail. Prescreened opt-out only covers credit and insurance offers tied to the credit bureau lists. Local business mailers, charity appeals, political mail, and anything from a company you've done business with – none of that is affected. DMAchoice.org is a separate tool for direct marketing mail.

I opted out, but I'm still getting offers. What's happening?

Give it 60 days. Offers that were already in production when your opt-out was processed will still arrive – the mailing pipeline doesn't stop mid-run. If the mail's still coming after the 60-day window, contact the credit bureaus directly.

Will opting out stop the calls I get after applying for a mortgage?

It helps, but it's not the whole solution. Those calls come from "trigger leads" – when you apply for a mortgage, lenders can buy data about the inquiry within hours. Congress addressed this directly with the Homebuyers Privacy Protection Act, which took effect in March 2026 and restricts credit bureaus from selling mortgage trigger lead data. Prescreened opt-out adds another layer, but the law is now the main protection.

Is 1-888-567-8688 a real number?

Yes, 1-888-567-8688 is a real number. It’s operated by all four major credit bureaus, verified by the FTC, and listed on each bureau's website. Worth knowing: the system doesn't make outbound calls. If someone calls you claiming to be from this number, hang up.