US consumer watchdog agency reveals that top scams of 2024 led to losses of $12B

The US Federal Trade Commission (FTC) says top scams, including imposter fraud, identity theft, and fake crypto investments, cost consumers more than $12 billion in 2024 – over $2 billion more in losses than the previous year.

Image by Carles Mateo Aguila | Shutterstock

The US Federal Trade Commission (FTC) says top scams, including imposter fraud, identity theft, and fake crypto investments, cost consumers more than $12 billion in 2024 – over $2 billion more in losses than the previous year.

The FTC released its annual Data Book for 2024 this week, categorizing the top-rated scams, how much money victims lost, and the method of contact, tracking the complaints from years past through to 2024.

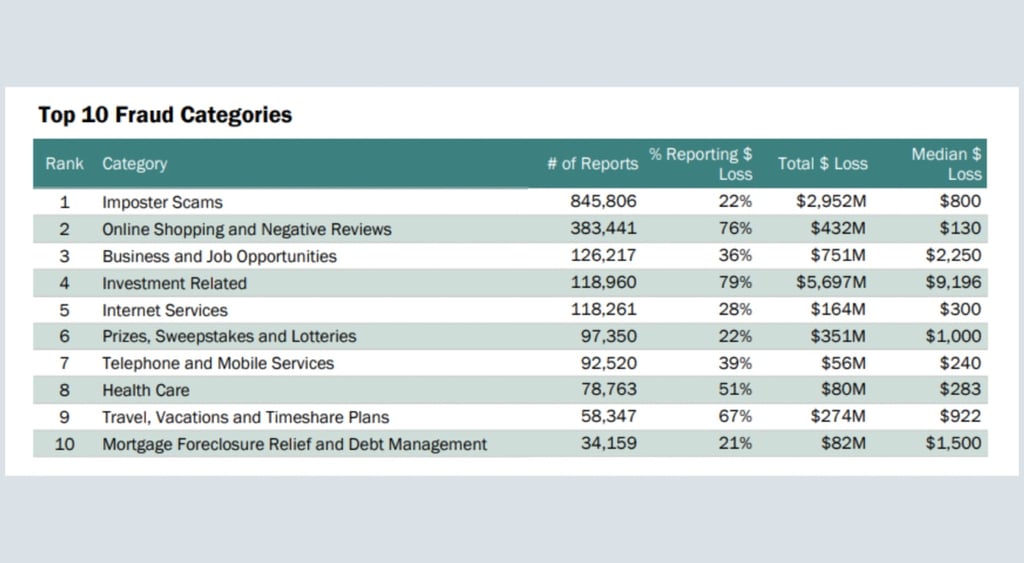

For those reporting money losses, investment scams led to the most losses, impacting one out of three people in 2024. The numbers increased about $1 billion yearly, jumping from $3.8 billion in 2022 to a total of $5.7 billion in investment losses in 2024.

In 2024, 79% of those who lost money in an investment scam reported an average loss of $9,000, far surpassing the median loss of just under $500 from all scams reported to the FTC.

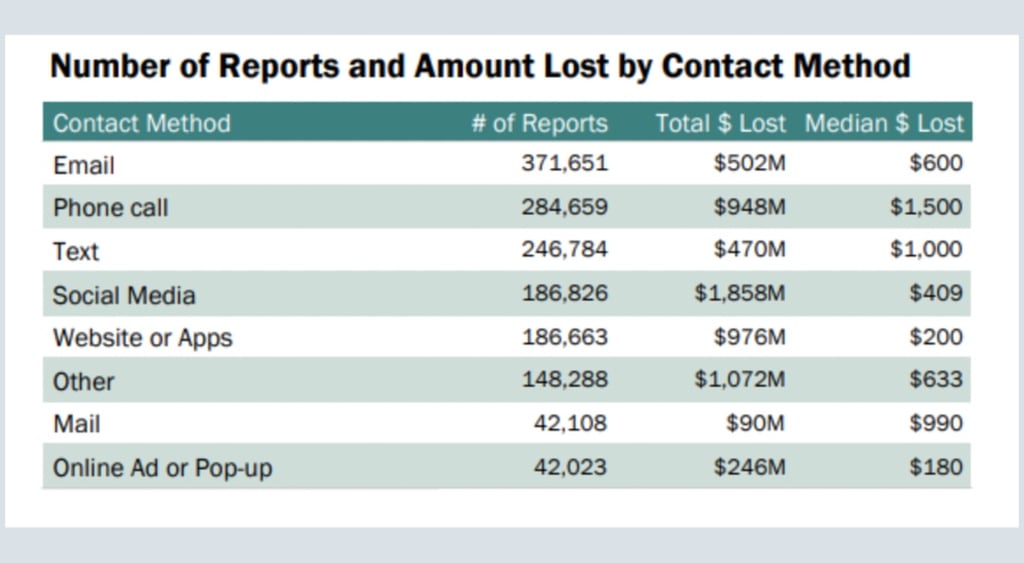

A whopping 70% of scam victims also reported losing money more often when contacted on a social media platform. Overall, losses in that category were about 1.9 billion in 2024.

The statistics come from over 6.47 million complaint reports submitted by dozens of consumer watchdog agencies, including federal, state, local, and international law enforcement agencies, the Microsoft Corporation Cyber Crime Center, the FBI’s Internet Crime Complaint Center (IC3), the US Better Business Bureau, and all Attorney General state offices across the nation.

The reports are then aggregated by the Consumer Sentinel Network (Sentinel), a secure, FTC-backed online database available only to law enforcement, and then disseminated to the public annually.

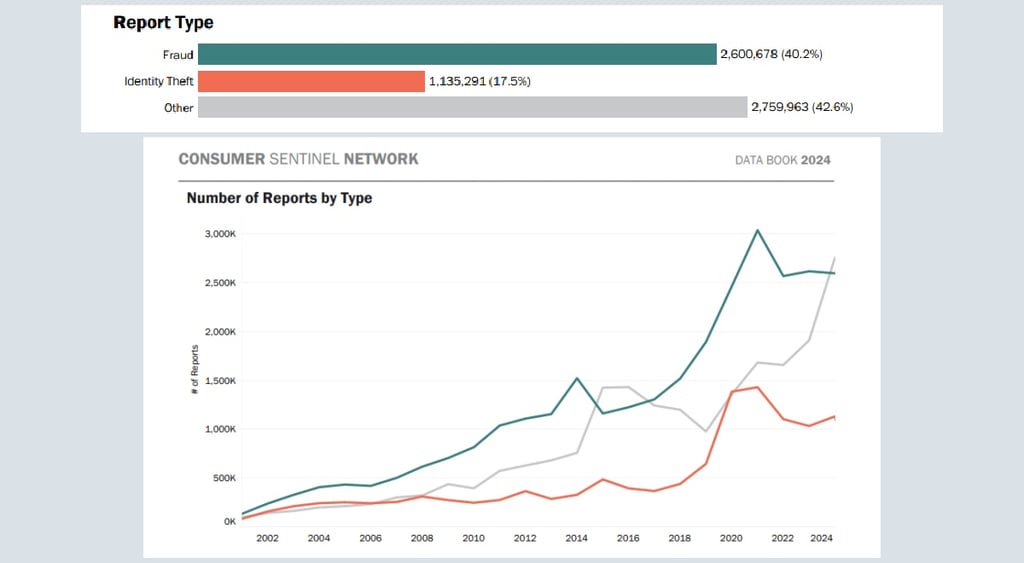

Sorted into 29 top categories, the FTC found that in 2024, 40% of all reports were related to fraud. Moreover, 18% of consumers reported being victims of identity theft, and another 43% of reports were a combination of various other scams such as imposters scams, internet services scams, and foreign money offer scams.

The Sentinel report showed that bank transfers and payments accounted for the highest aggregate losses in 2024, at over $2 billion, followed by cryptocurrency, at $1.42 billion. Overall, more than $5 billion in losses were said to be related to some type of investment scam.

Meanwhile, misuse of credit card accounts or applications for new credit cards was listed as the most common payment method in consumer fraud reports (nearly 450,000 reports), most often obtained through identity theft, followed by fraudulent use of payment apps.

The FTC said the reports showed personally identifiable information would be used to create or hijack email or social media accounts, online shopping or payment account, to break the law or avoid the police, to get insurance or medical care, or to open or use a person’s securities or investment account without their permission.

Furthermore, there were nearly 850,000 imposter scam complaints in 2024, representing 13% of all reports and bilking consumers out of close to $3 billion, the FTC said.

“An imposter scam is when someone pretends to be a trusted person to get consumers to send money or give personal information,” the FTC said.

Criminals posing as a government agency or employee, a friend or relative with an emergency need for money, a romantic interest, a computer technician offering technical support, or a charity or company, made up the bulk of imposter scams.

Not surprisingly, email was the most common contact method for 25% of fraud reports, followed by phone calls, texts, and then social media.

And, of those people who reported their age, the data book noted that individuals aged 20-29 reported losing money to fraud more than older people. Still, those over the age of 70 reported losing the most money of all age groups.

States with the highest per capita rates of reported fraud in 2024 were Florida, Georgia, Delaware, Nevada, and Maryland, while top states listed for the most identity theft were Florida, Georgia, Nevada, Texas, and Delaware.

Even so, the state of California reported the most consumer losses out of any state at over $1.6 billion.

“While the FTC does not intervene in individual consumer disputes, its law enforcement partners – whether they are down the street, across the nation, or around the world – can use information in the database to spot trends, identify questionable business practices and targets, and enforce the law,” the agency said.